Make time to keep these journals current to track business expenses and receipts at any given time. So, when bidding on construction projects, each cost must be carefully examined by checking current market prices to win the bid. The construction industry is subject to economic, political, weather, and seasonal fluctuations.

Setting up a Construction Bookkeeping System

First and foremost, whether you’re talking about construction accounting or any other business, separate your personal and business finances by opening a separate business bank account. This will make it much easier to account for your business expenses during tax time. By leveraging digital invoice capture and automated approval workflows, you can streamline your invoice processing and payment cycles while eliminating the need for manual data entry. Digitizing your invoice management system allows you to capture invoices electronically, automatically extract data from them, and route them for approval without human intervention. With an automated approval workflow, you can accelerate the payment process and ensure that invoices are approved and paid on time.

Construction Management: Key Roles and Tools

- The decentralized nature of the industry sees production scattered, occurring in multiple locations.

- To remain on schedule and budget, precise bookkeeping for construction companies is essential.

- In many cases, you need to have your financial records for at least three to seven years (varying by state and type of record) so losing them would cause a lot of problems.

- Working with a certified bookkeeper or accountant specializing in construction accounting can greatly benefit your business.

- On the other hand, if it’s super easy to use but doesn’t provide the flexibility you need, you should consider trying a different one.

Implementing bookkeeping for your construction business may seem overwhelming, but it’s doable. Doing so allows you to easily retrieve any document whenever you need it, save time and effort searching through paper files, and ensure that all your records are up-to-date and accurate. When embarking on a project, it’s important to break down the costs into manageable categories to ensure the budget is well-managed. The project costs can be divided into several categories, such as materials, labor, equipment, and permits.

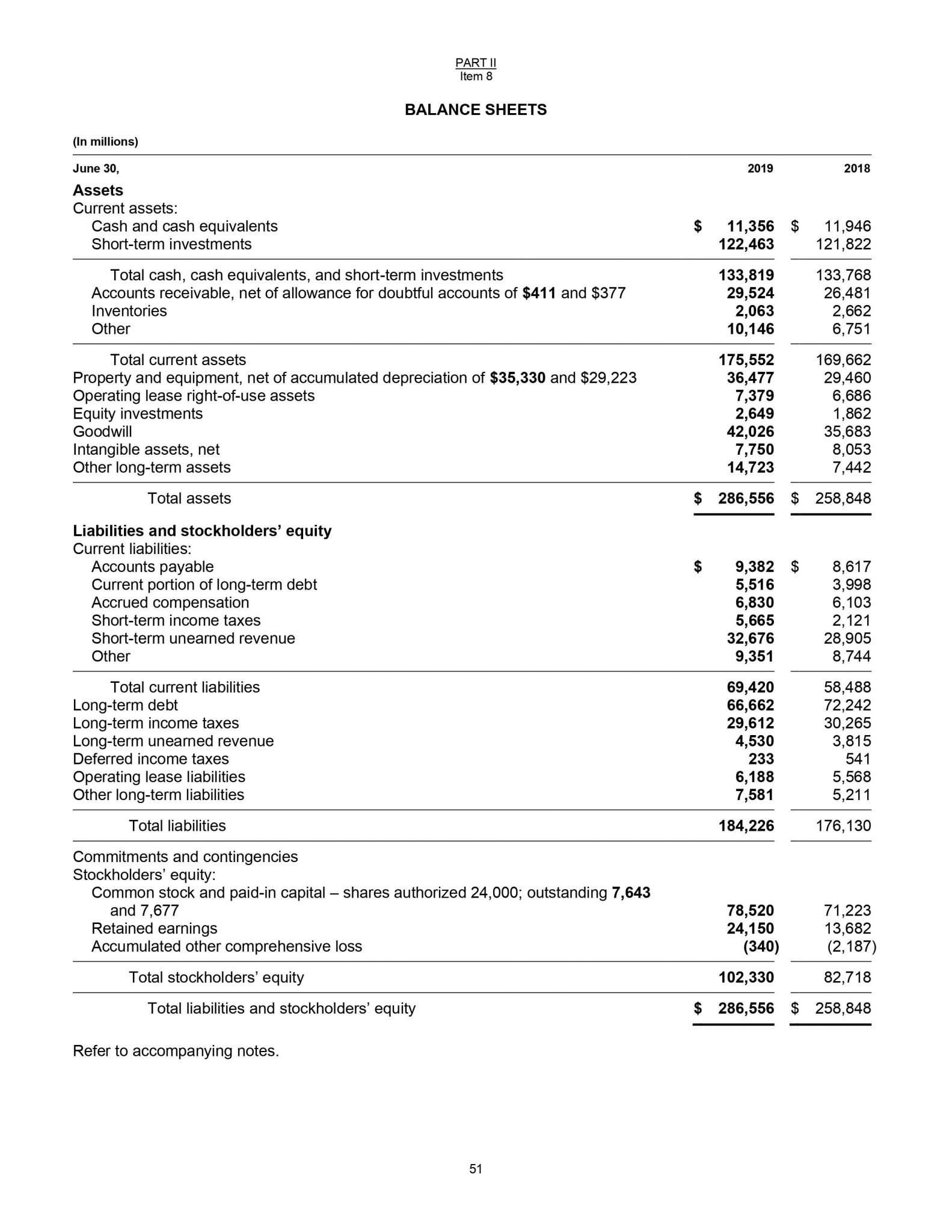

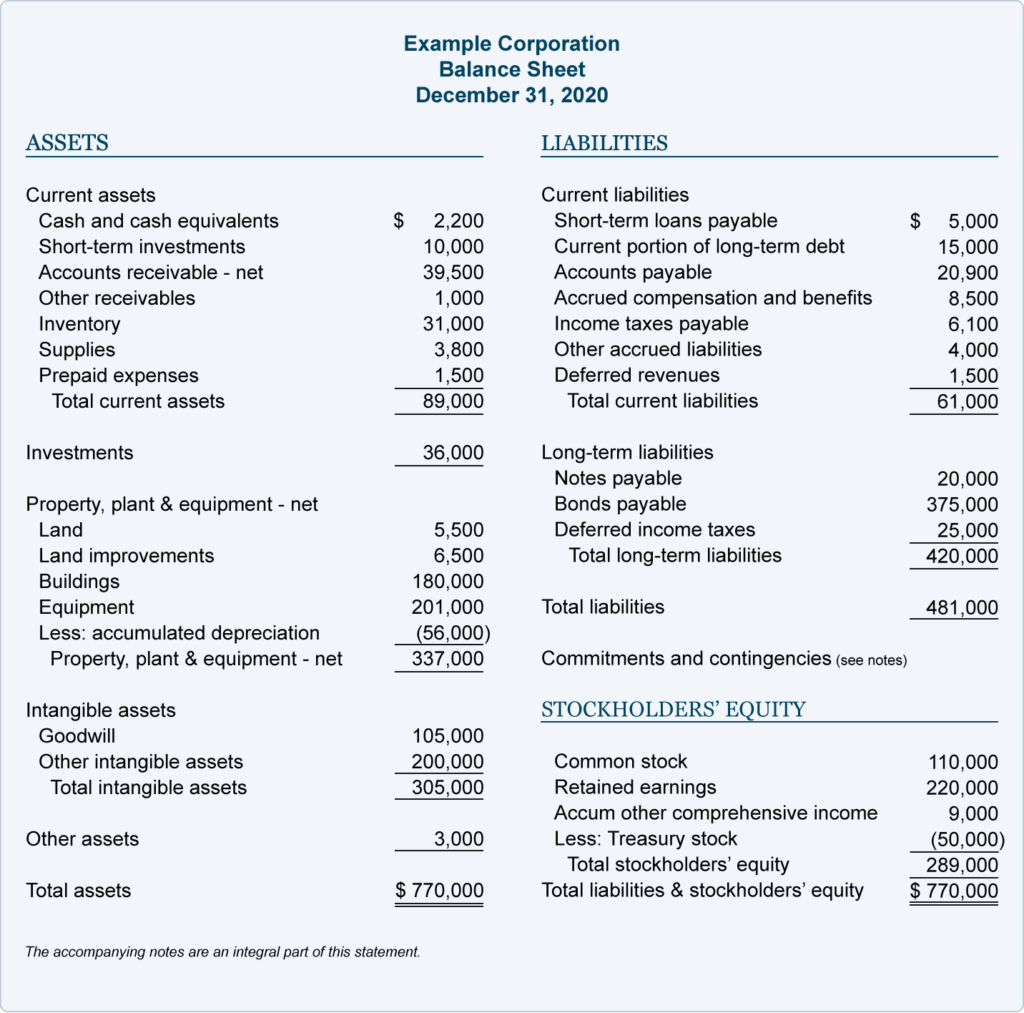

Best Practices in Developing a Chart of Accounts for a Construction Company

Whether you decide to do job costing manually or using software, the same steps apply. Apart from giving you insight into where your money is going, receipts also serve as proof of your business expenses in case you ever get audited. Here are ten tips that can help to simplify and improve the way you handle construction bookkeeping. Companies must ensure compliance with standards such as IAS 16 or ASC 360, which govern the recognition and measurement of fixed assets.

Why is a chart of accounts needed?

By subscribing you agree to with our Privacy Policy and provide consent to receive updates from our company. Meet a Knowify expert, get your questions answered, and start your journey today toward organized, profitable projects with Knowify. How to Use Construction Bookkeeping Practices to Achieve Business Growth Watch how leading ENR 400 contractors have leveled up their workforce planning by leaving their spreadsheets behind.

- Bookkeeping for construction companies is based on construction contracts, which typically last longer compared to other industries since projects can take months or years to complete.

- To effectively manage these variable expenses, you can use FreshBooks Project Accounting Software which lets you track project financials and create reports quickly and easily.

- The transition from construction to fixed status marks a pivotal moment in asset management.

- This enables them to access project information and communicate with other team members from anywhere.

- Progress billing is one of the most widely used methods in construction, particularly for long-term projects.

Retainage is a common practice in the construction industry where a percentage of the contract amount is withheld until the project is completed. This approach protects clients but can negatively affect cash flow for contractors. Properly accounting for retainage is essential for accurate financial reporting and effective cash flow management. This guide covers key aspects of construction bookkeeping, including the role of a construction bookkeeper, recording expenses, and industry-specific accounting methods. By mastering these practices, construction companies can gain better control of their financial performance and reduce inefficiencies in managing costs.

Turn your receipts into data and deductibles with our expense reports that include IRS-accepted receipt images. Job costing is critical for construction companies to be profitable and project successful. Contract retainage is a portion of the final payment held back until later to ensure the contractor has completed the project thoroughly and correctly.

- However, smaller companies or those with shorter projects may prefer the completed contract method for its simplicity.

- There are four revenue recognition methods, but for the sake of this guide, we’re going to focus on the percentage of completion method (POC), which is what most contractors end up using.

- These may include administrative salaries, office rent, utilities, and other general operating expenses.

- To manage cash flow effectively, companies need to track their cash inflows and outflows and forecast their future cash needs.

There are many software options available that are specifically designed for construction companies, such as QuickBooks https://www.merchantcircle.com/blogs/raheemhanan-deltona-fl/2024/12/How-Construction-Bookkeeping-Services-Can-Streamline-Your-Projects/2874359 for Contractors, Foundation Software, and Sage 100 Contractor. To simplify this process, many construction companies use payroll software that can automatically calculate wages and taxes. These programs can also help with other aspects of payroll management, such as generating pay stubs and handling direct deposits. In construction, several billing methods are commonly used, each tailored to different types of projects and contractual arrangements.

Additionally, you gain better visibility and control over your invoicing process, which helps you optimize your cash flow and improve your supplier relationships. Accounting software makes it easier to keep your records accurate, neat, and tidy. With accounting software, you simply enter the data and the software puts it where it needs to go.